Digital PFIC

© 2026 PwC. All rights reserved.

PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity.

Please see www.pwc.com/structure for further details.

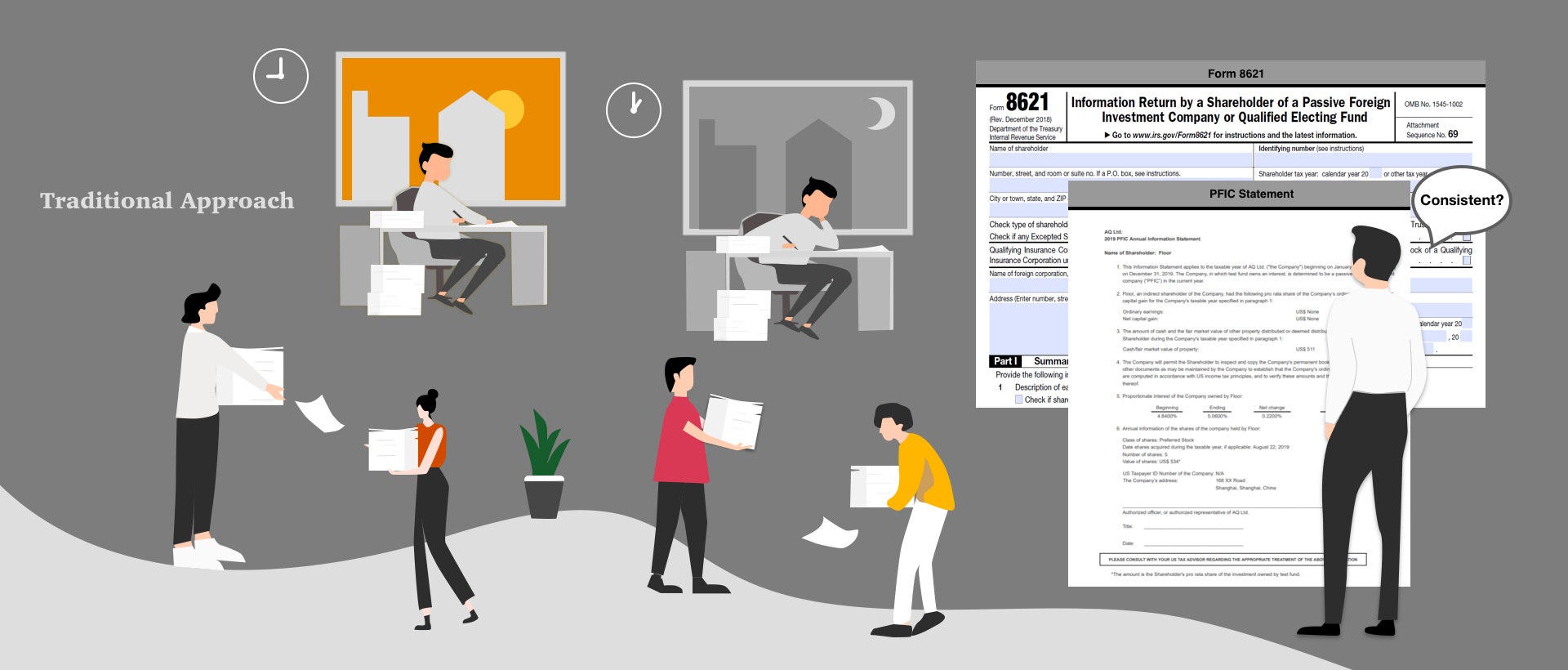

Certain US persons may become subject to the passive foreign investment company (PFIC) regime if they own an interest in non-US companies that invests primarily in passive investments. The PFIC regime imposes obligations for US persons to report taxable income and comply with certain reporting requirements.

A foreign corporation is a PFIC, if 75% or more of its gross income considered passive income, which generally includes dividends, interest, royalties, rents, annuities, and capital gains, or 50% or more of the company’s assets are investments that produce or are held for production of passive income. Various special rules apply to perform this calculation.

The evaluation of PFIC status is performed on a quarterly and annual basis.

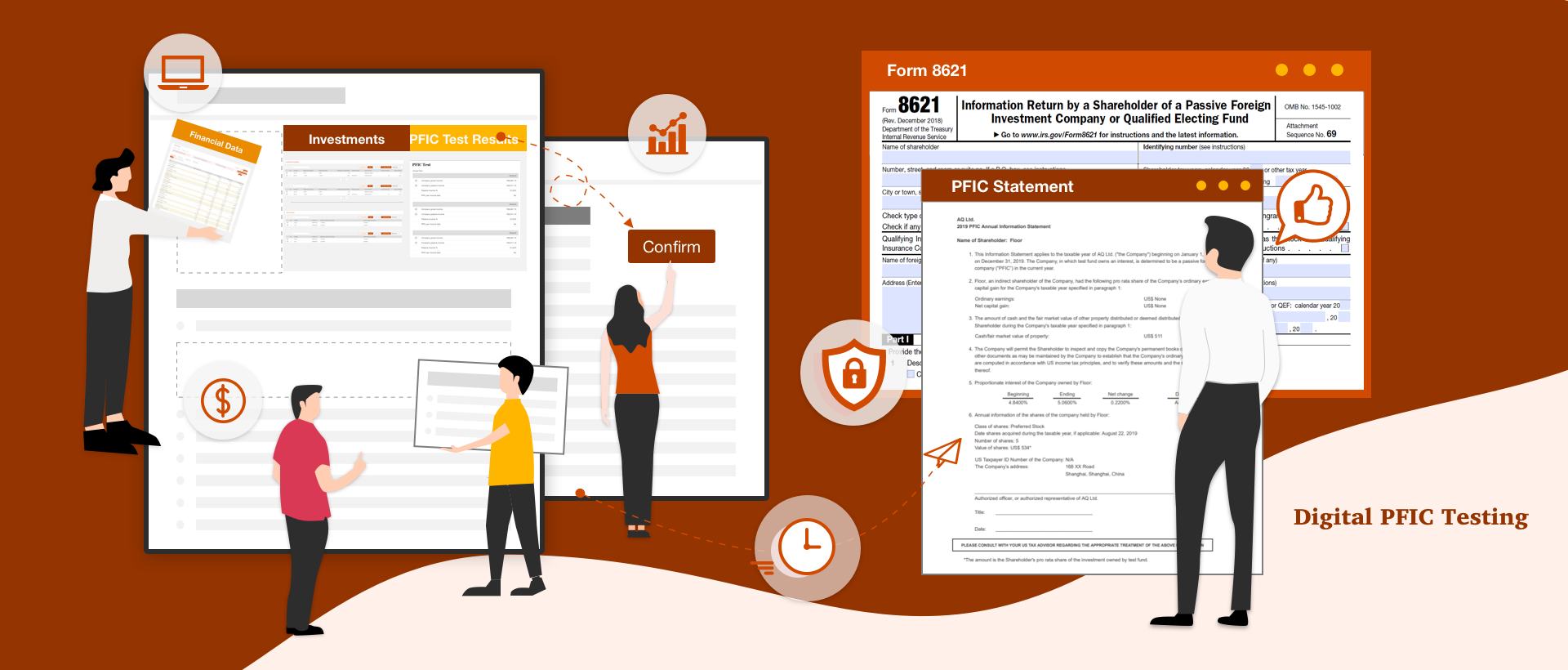

Investment funds and other investors, and/or portfolio companies input financial and other data into the online Digital PFIC Testing platform.

After the financial and other data is validated, PwC tax experts, via the Digital PFIC Testing platform, review the PFIC assessments and confirm the results.

Finally, the PFIC reports and forms are generated and made available to investment funds and other investors, and/or portfolio companies.